All Categories

Featured

Table of Contents

guarantee a stream of revenue for the remainder of the annuitant's life, nonetheless long that might be, or for the life of the annuitant and their partner if they purchase a joint life time annuity. Missing a joint-and-survivor provision, however, the annuitant is the only one that can benefit. Think of it as an individual contract designed to profit the annuitant alone.

The more money that was placed in, and the later the repayments were started, the larger those payments will certainly be. The contract terminates at fatality. If the annuitant purchases a life time annuity, it suggests they can't outlive their revenue stream, but it additionally implies the beneficiaries won't reach assert the benefit after the annuitant's gone., additionally called, pay over a limited time period - Single premium annuities.

Because of this, they may perhaps outlast their advantages. On the flipside, though, if they pass away before the agreement runs out, the cash can pass to a designated beneficiary. pay at an ensured rates of interest but use a reasonably small price of return. If you acquire a repaired annuity, you'll know what you're entering regards to development.

This sets you back additional but gives the beneficiary the greater of these two payouts: The contract's market price. The total of all payments, when fees and withdrawals are deducted. It is very important to note that the size of the costs being returned will be less than it was originally, depending on just how much of it the initial annuitant has actually taken in payments.

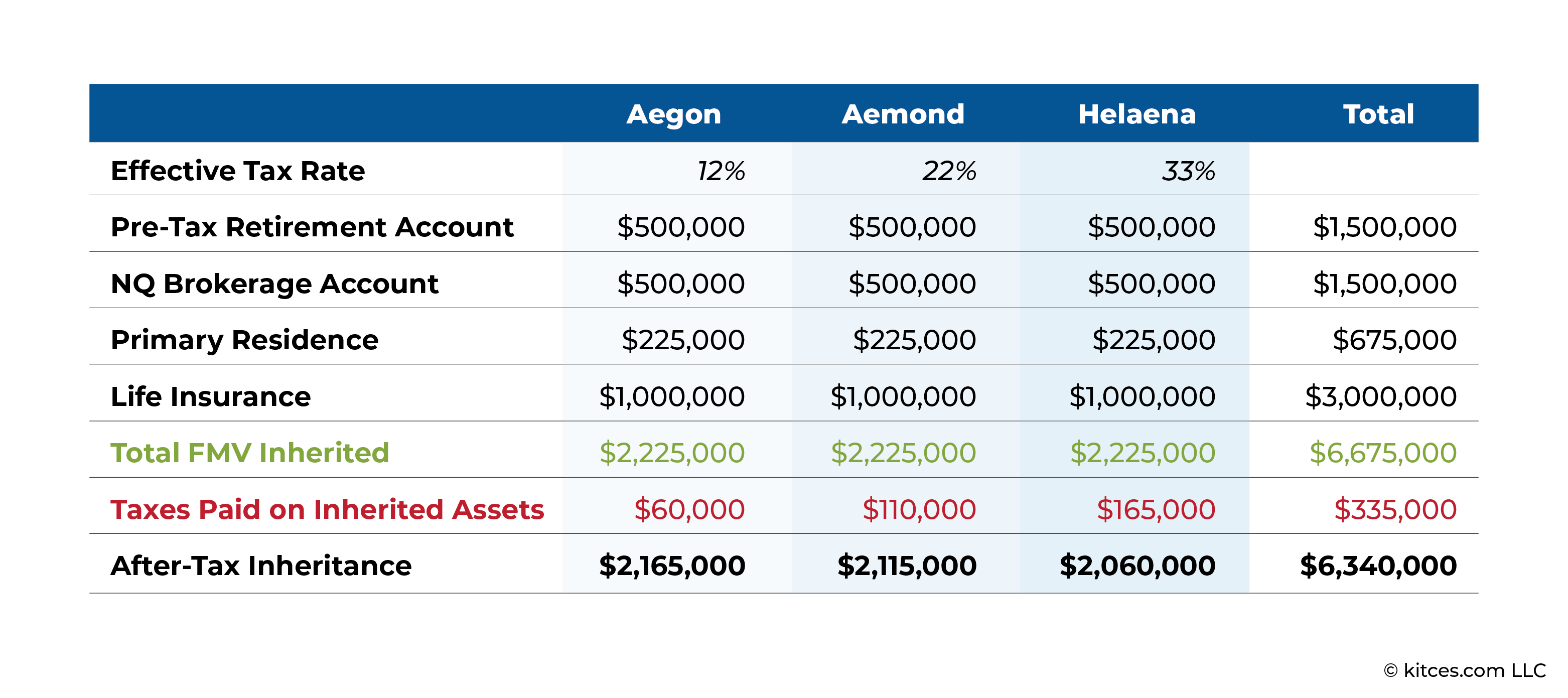

How does Joint And Survivor Annuities inheritance affect taxes

are optionalclauses in an annuity agreement that can be made use of to customize it to specific demands. They come at an additional price due to the fact that they typically supply an additional level of defense. The even more cyclists bought, the greater the cost is to pay: Each cyclist commonly costs in between 0.25% and 1% every year.

Without such a rider, the staying money would go back to the insurance policy company, to be merged with funds for other life time annuity owners that might outlast the amount they would certainly invested. It wouldn't go to the successors. (This is a trade-off for the insurance provider since some annuitants will outlive their investments, while others will certainly die early.

It costs extra due to the fact that the insurance policy firm requires something to balance out the money it could otherwise utilize for its swimming pool. Is this added price worth it? If the annuitant remains in health and assumes they could use up all or the majority of the costs prior to they pass away, it might not be.

Under this cyclist, the insurance firm tapes the worth of the annuity every month (or year), then uses the greatest number to establish the advantage when the annuitant dies - Annuity payouts. An SDBR secures beneficiaries of variable annuities against market fluctuations: If the value happens to be down at the time of fatality, the recipient still obtains the top-line amount

Yet the securities behind the lottery payout are backed by the united state government, which really makes them much safer than any type of privately backed annuity. Electing to take annuitized installment repayments for lottery game jackpots can have a couple of benefits: It can guard versus the temptation to overspend or exhaust on obligations, which may result in economic problems or even personal bankruptcy in the future.

Tax rules for inherited Annuity Beneficiary

If you get an annuity, you can establish the terms of the annuity contract, choose what kind of annuity to buy, choose whether you want cyclists, and make other choices. If you acquire an annuity, you may not have the same alternatives, specifically if you weren't a spouse with joint ownership.

An annuitant can call a main recipient and a contingent beneficiary, but additionally can name more than one in either classification. There's actually no limit to the number of primary or contingent recipients that can be named.

And (sorry, pet enthusiasts), Dog or Floofer can not be named as a beneficiary. Neither can a pet rock or other inanimate item. Yes. An acquired annuity can offer cash for the beneficiary to settle significant costs (such as pupil financial debt, a mortgage, health-care prices, and so on). If you decide to sell your inherited annuity, you can do so in one of three methods: You can market all your arranged payments for the remainder of the annuity agreement term and obtain a lump-sum repayment in exchange.

As an example, if you have 15 years continuing to be on your inherited annuity, you can offer the initial 5 years and get a round figure for that. After those five years are up, settlements will return to. If you prefer not to wait for payments to launch once again, however you need some money now, you can offer a portion of each repayment and obtain a round figure.

Inherited Long-term Annuities taxation rules

Depending upon your credit, the regard to the finance and various other factors, you might end up paying practically as much in interest as you got via the financing. As an example, a 30-year mortgage worth $200,000 would certainly cost you an overall of more than $343,000 when all is said and done.

The solution to this question depends on a number of aspects. Amongst one of the most important is when the annuity was acquired. If you acquired an annuity before your marriage, it may be considered your separate property and not eligible to be separated by the court. An annuity acquired during the marital relationship may be checked out, lawfully, as area residential property and topic to department.

Splitting an annuity in a separation can have serious tax obligation repercussions. Some divorce lawyers might not know the threats of doing it incorrect. It's important that you likewise talk to a monetary advisor about the prospective implications in crafting any negotiation. If you own a qualified annuity possibly it became part of a pension plan, 401(k), or other employer-sponsored retired life plan moneyed with pre-tax dollars you will certainly require a (QDRO).

This means that the beneficiary's share of the annuity earnings would certainly pass on to successors if the beneficiary dies prior to the contract owner., was passed in 1974 to shield retired life savings and uses particularly to retirement strategies funded by private staff members.

Deferred Annuities death benefit tax

A non-designated recipient is an entity such as a charity, count on, or estate. Non-designated recipients go through the five-year regulation when it involves annuities. So, if you acquire an annuity, what should you do? The answer depends upon a selection of factors linked to your economic circumstance and individual objectives.

If so, you could take into consideration taking the cash simultaneously. There's absolutely peace of mind in owning your very own home; you'll have to pay residential or commercial property taxes, yet you won't need to bother with proprietors elevating the rent or sticking their nose in your company. (We all understand how much enjoyable that is.) The tax obligation responsibility and charges you incur by moneying in your annuities at one time can be offset by the revenues from that brand-new organization or the admiration worth on a home.

{kind=link}

Table of Contents

Latest Posts

Decoding How Investment Plans Work A Comprehensive Guide to Fixed Annuity Vs Equity-linked Variable Annuity What Is Fixed Income Annuity Vs Variable Annuity? Advantages and Disadvantages of Annuity Fi

Understanding Financial Strategies Everything You Need to Know About Financial Strategies What Is the Best Retirement Option? Benefits of Choosing Between Fixed Annuity And Variable Annuity Why Choosi

Highlighting the Key Features of Long-Term Investments A Comprehensive Guide to Fixed Vs Variable Annuity Breaking Down the Basics of Immediate Fixed Annuity Vs Variable Annuity Pros and Cons of Vario

More

Latest Posts